“It’s always darkest….before it turns pitch black.” — Chairman Mao

“Watched water doesn’t boil.” — Unknown

“Make sure the light at the end of the tunnel isn’t an oncoming train.” — Peter Lynch

'Twas the week before Christmas and not a surprise, I was looking for excuses not to do the inevitable…fight the legions at the mall and go shopping.

Much to delight, my Vikings were on TV against Jeff Saturday’s Colts, eager to avenge the humiliation they suffered against the here-to-for hapless Lions.

I say “my Vikings” because I grew up in Minneapolis and while four Super Bowl losses has buried my outward passion for them, deep down, they’re still my true love.

Was there anything better than the “Purple People Eaters” with Alan Page and Carl Eller chasing quarterbacks all over creation?

Or the stoic Bud Grant on the sideline not being able to tell if the Vikings were up three touchdowns or down two touchdowns? (he famously told his players not to spike the ball after a touchdown and “act like they’d been in the endzone before.”)

“Scrambling” Fran Tarkenton, Chuck Foreman, and Fred Cox (the pointed toe kicker, dentist and inventor of the NERF football.).

Yes, there were the disappointments and the embarrassments…the aforementioned Super Bowl losses, the Roger Staubach to Drew Pearson Hail Mary, Jim Marshall running the wrong way to score for the opposing team, fellow Minnesotans dressing up as Vikings (and even axe-throwing like them)…all painful but part and parcel with unconditional love.

All of this leads us to Saturday’s matchup between Minnesota and Indianapolis and me plopped down in front of my TV to root on the Vikings…SKOL!

Much to my dismay, before I could even enjoy a bowl of popcorn, the Vikings were down 33–0 at half, which included not one, but two “pick sixes.” I basically had no excuse to continue to watch the train wreck so I went out and did what I should have done in the first place…I went Christmas shopping.

I didn’t bother looking at my ESPN app because there was no need, there wasn’t a prayer the Vikings were going to come back from nearly a five touchdown deficit. By-the-way, in the over 100 year history of the NFL, no TEAM has ever come back from being behind by 33 points.

So later, while casually looking at scores on the elliptical, when I saw that Minnesota won 39–36 in overtime, I had to do a triple take, with me seriously questioning whether I was processing this correctly.

The lesson learned…the biggest opportunities are where people have already thrown in the towel.

While my passion for the Vikings has been with me as long as I can remember, my passion for online learning began when I realized what the Internet could do to democratize education…lower the cost, increase access and ultimately improve the quality.

The biggest investment opportunities are where there is a problem, the greater the problem, the bigger the opportunity. In a Knowledge Economy and Global Marketplace, it was hard to imagine a bigger problem or opportunity than how to more effectively educate our population.

Early pioneers included Apollo Group, which reached a $15 billion Market Cap at its peak, and whose NASDAQ symbol (APOL) we used to say stood for “A Professor OnLine”. UNext was another online education company that had me at “hello” because of the vast potential. Both fell short of what I had dreamed could happen for various reasons. Alas, being too early is the same as being wrong... and the pioneers get all the arrows.

But, the ones that survive get all the land! Hence, I continued to forge ahead looking for online learning enterprises that could provide high quality and low cost solutions to the Market. Additionally, VC funding to digital learning companies skyrocketed from $500 million in 2010 to over $20 billion in 2021.

Chegg (what comes first, the Chicken or the Egg), 2U and Course Hero (now Learneo) were online learning companies that we backed over 10 years ago that have driven high return on education (ROE) and high return on investment (ROI).

Imagine my delight when co-founder of Coursera Daphne Koehler came into my office in 2012 to explain the radical concept behind her new business. What if you could Partner with the World’s best universities and professors to provide FREE online courses? Like other successful FREEMIUM models, you monetize the platform downstream by creating massive network effects and convert a small percentage to paying customers (we had invested in other successful FREEMIUM models such as Facebook, Twitter, Spotify and Snap, so why wouldn’t that work here?)

Coursera's thesis was always student-first: the platform would benefit its university partners to achieve broader scale, and the earned credentials would play a key role in corporate learning and in hiring.

Andrew Ng’s Vision for Coursera’s Long-Term Model, 2013

Today, over 113 million learners from around the world access the platform to gain knowledge, to earn certificates and get diplomas from the top universities.

The Coursera ride has been amazing for most of the past decade, with over 100 million students, 200 universities and 5000 courses on the platform. And while the vast majority of the students on Coursera don’t pay a dime, the company has built a business with over $500 million in revenue and nearly a $2 billion market cap today.

Estimates are for the company to do $520 million in revenue in 2022, up from $415 million in 2021 and estimated $623 million in 2023. Coursera is losing money currently but has $424 million in cash and could turn profitable if it prioritized that and sells at 1.3x 2023 sales.

That’s the good news. The bad news is that while Covid was a major accelerator of its business (and permanent accelerant for the industry), it created a stock that was probably ahead of itself, stubbed its toe a bit and had challenging comparisons.

The result is that many investors have thrown in the towel, and Vegas, oops, I mean Wall Street has put the odds as remote that we are going to see big investment return from COUR anytime soon. The way I see it is despite what the score says, I like the fundamentals of the company and the open ended potential…and the low stock price.

(Disclosure: GSV owns shares in Coursera)

Market Performance

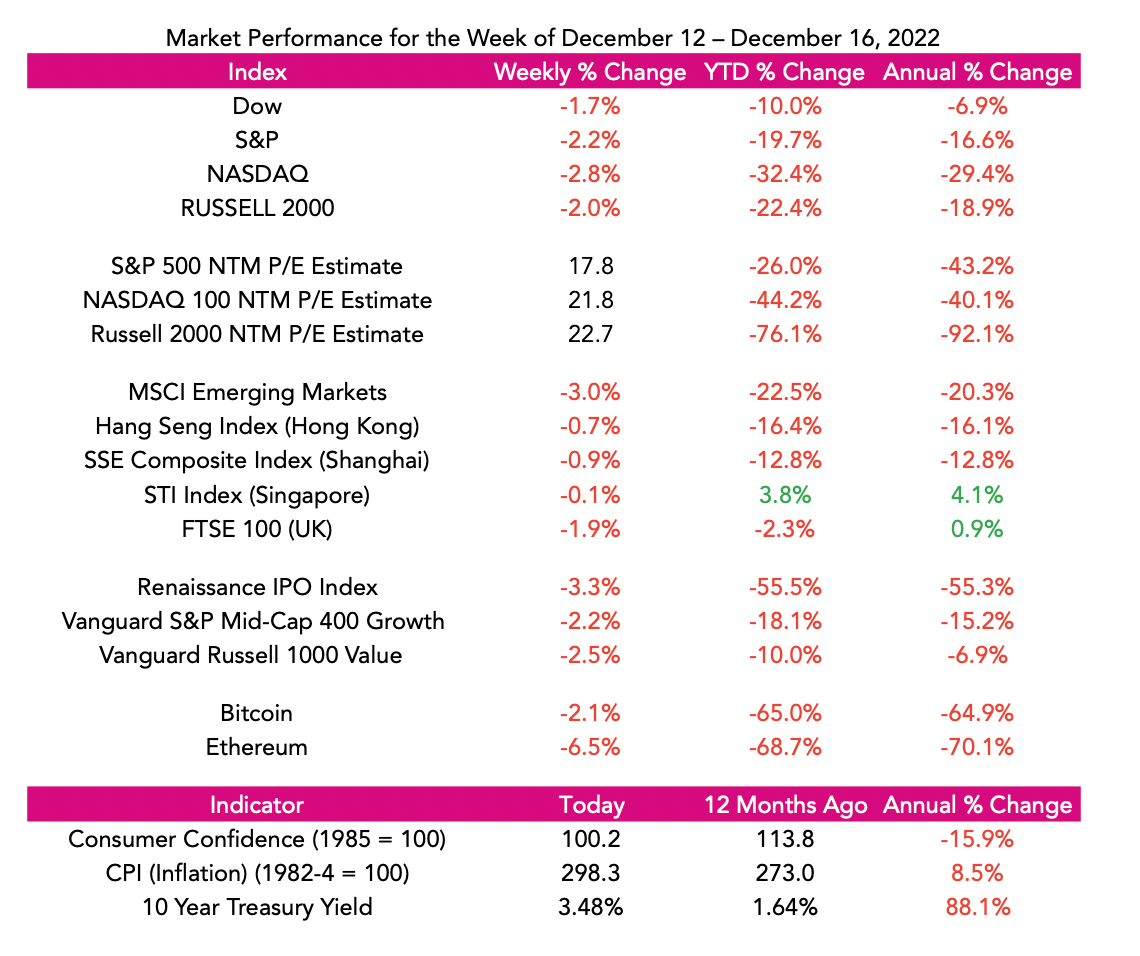

“Doom” and “gloom” summarize market sentiment, accentuated by stocks falling for the second straight week. The Dow was down 1.7%, the S & P fell 2.2% and NASDAQ dropped 2.8%. Year-to-date, the S & P 500 is down nearly 20% and the tech laden NASDAQ has fallen more than 30%.

While the annualized Consumer Price Index “only” rose 7.1% last month, the Fed, the ECB and the Bank of England all raised rates. Since January, short term Treasuries have risen from .7% to 4.2% and in correspondence to that, many high growth, high multiple stocks are down 50–90%.

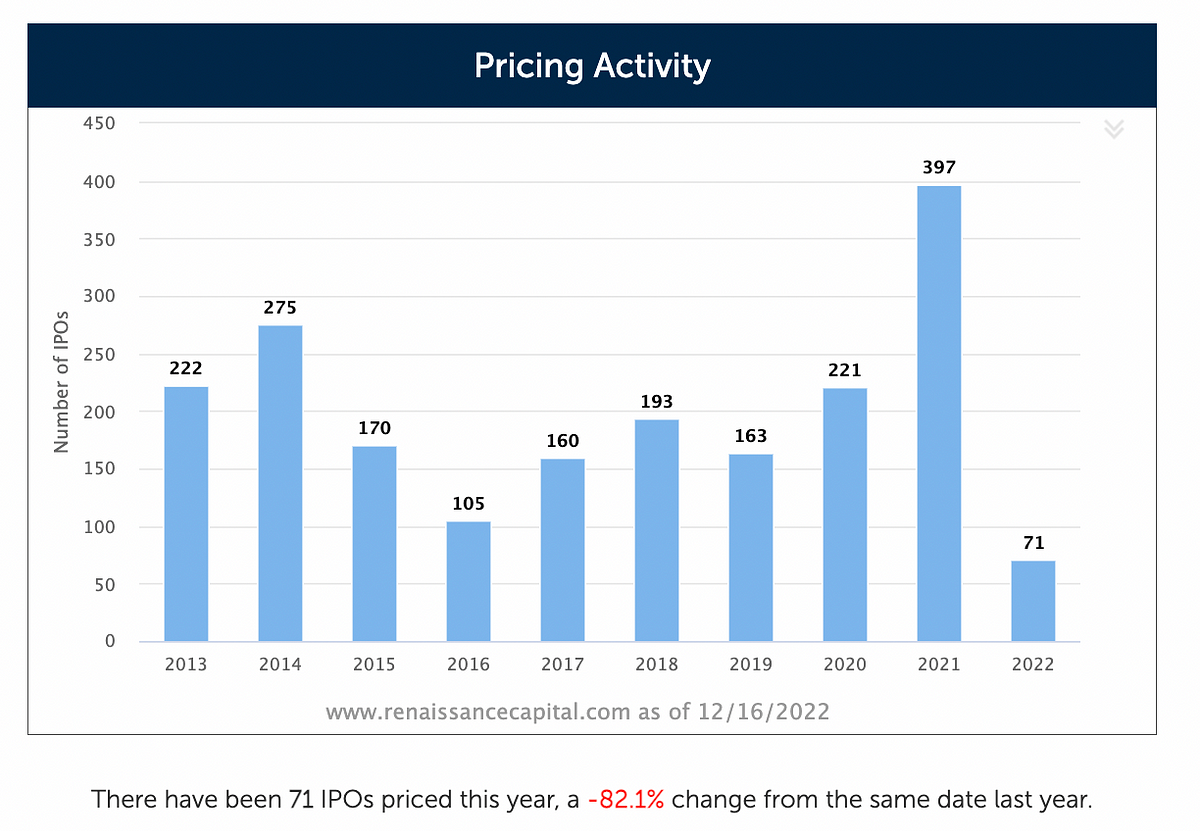

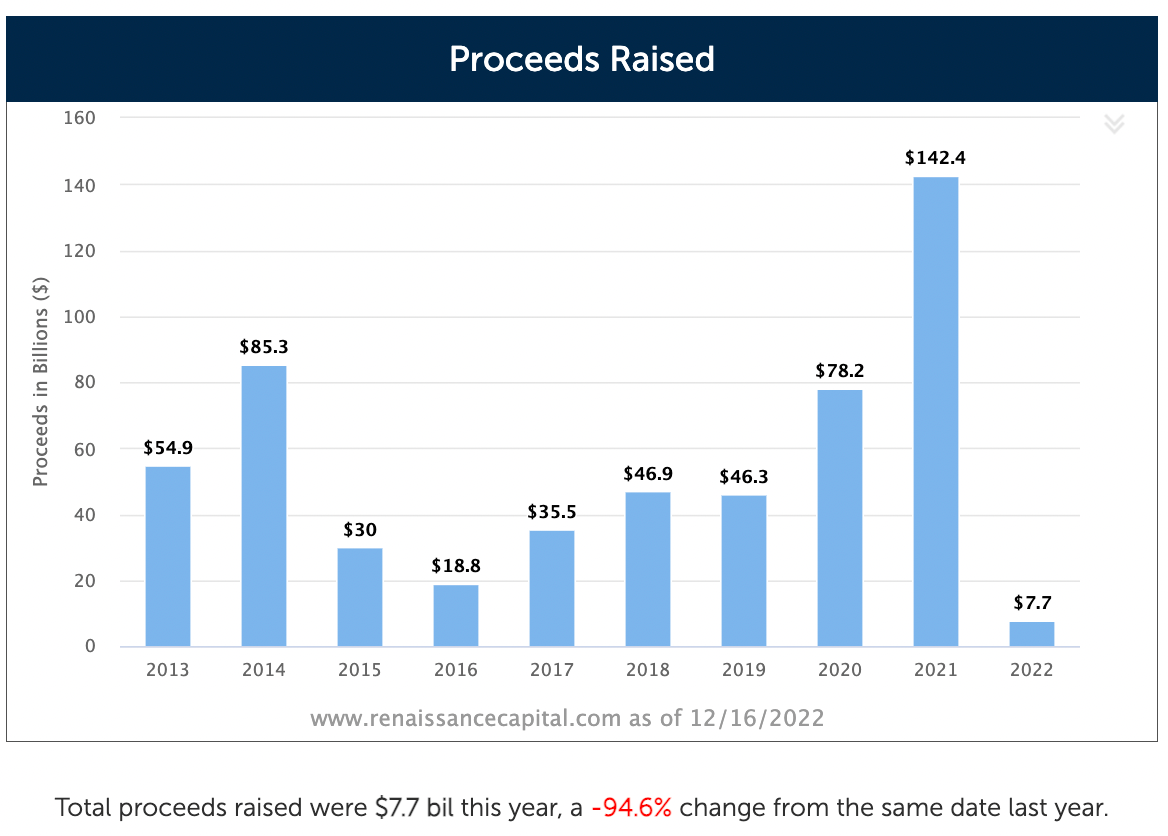

IPO’s, which are the fresh oxygen for growth investors, will have its worst year since 2009 with just 74 companies going public in the U.S. raising approximately $8 billion.

Crypto, proxied by Bitcoin being off 67% in the past year, is facing existential challenges, with the former leader of that movement now enjoying the industry’s “nuclear winter” from a Bahamas jail.

Also, interesting from our perch was Microsoft’s $2 billion investment into the London Stock Exchange for 4% ownership. Microsoft will provide Data and Analytics as part of the deal. Brings back memories when Microsoft and Intel were early investors in NASDAQ.

With the world being BEARISH, and increasingly more so, that perks up our interest in being the opposite. To wit, if everybody is a seller, that’s reflected in share prices. Difficult times but opportunities abound.

GSV's Four I's of Investor Sentiment

GSV tracks four primary indicators of investor sentiment: inflows and outflows of mutual funds and ETFs, IPO activity, interest rates, and inflation. Here’s how these four signals performed this past week:

#1: Inflows and Outflows for Mutual Funds & ETFs

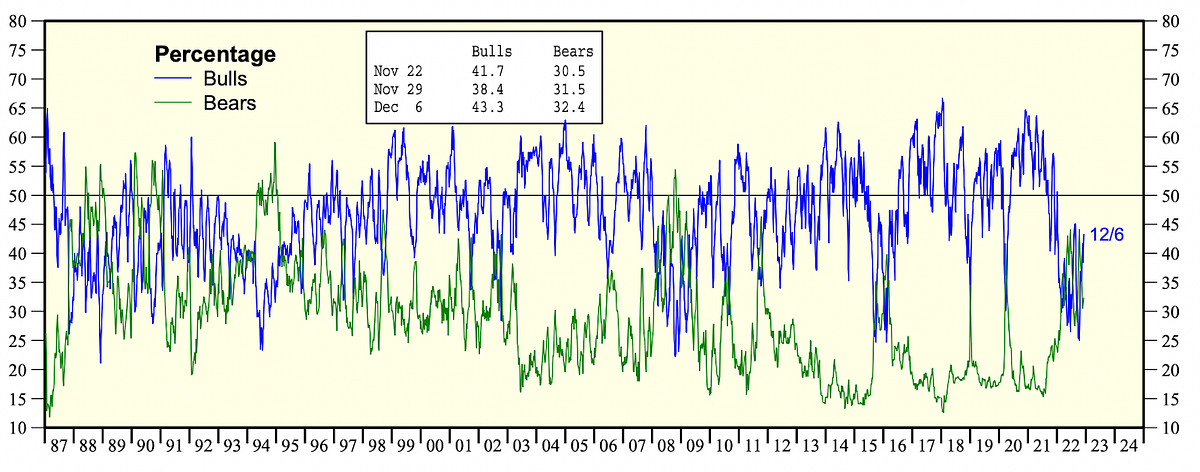

Total Equity Funds decreased from (-11.3) to (-15.0) from 11/23 to 11/30. Yardeni Research also published their annual bull/bear index…it’s looking like a toss-up for 2023.

2022 was the worst year for U.S. IPOs since 1990, while the global IPO market had its lowest amount of proceeds since 2016. Hopefully we have more news to report by this time next year.

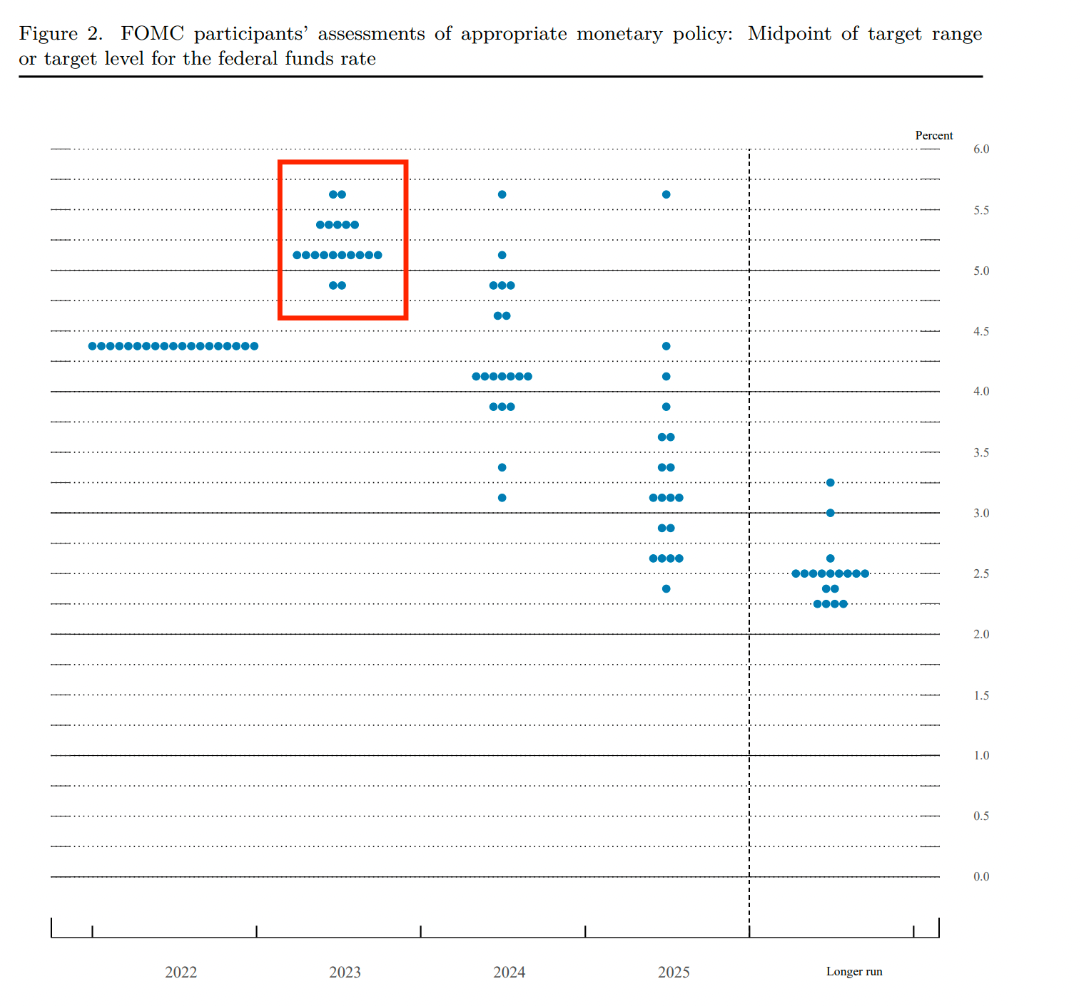

The Fed raised rates as expected by 50bps to a target range of 4.25–4.5%. What was more of a surprise is in the dot plot below. Before the meeting, the expectation was that the fed funds rate would peak at ~4.8% next year. Now, almost every FOMC participant expects rates to peak at greater than 5% in 2023.

#4: Inflation

Inflation came in surprisingly light for November 2022 — it came in lower than 65 of 67 economists surveyed by Bloomberg. Time will tell if this is a blip in the radar…or the beginning of brighter times ahead.

Chart of the Week

Chuckles of the Week

Video of the Week

Deepfakes are looking more and more real...

The GSV Big 10

This fall, we launched The GSV Big 10, synthesizing the news to bring you the top 10 stories and insights in learning and skilling. In case you missed it, here are some of last week’s top stories:

#1 Students turn to TikTok to fill gaps in school lessons

TikTok isn’t on a student’s syllabus, but it’s quickly becoming the world’s most important learning platform. The average TikTok user spends ~100 minutes on the app per day — that’s just as much time as on Twitter, Instagram, and Snapchat combined . Call it “Hollywood Meets Harvard” or Invisible Learning, one thing we know is TikTok is meeting students where they’re at.

#2 Google to Rival OpenAI’s ChatGPT? New AI Bot for Chats in 2023, CEO Claims to Use it for Search

The Empire Strikes Back? Google has owned the most valuable real estate on our screens for the past two decades — the search bar. Some have called ChatGPT an existential threat to Google. We expect to be hearing from Google’s DeepMind very soon.

#3 Opinion | Attacking Teachers From Every Angle Is Not the Way to Improve Schools

We definitely agree that attacking teachers is not the solution for improving schools. And we are sure that we need to reimagine how we create a system that attracts the best and the brightest into the teaching profession. The author says it starts with paychecks; we say it starts with aligning objectives, resources, and accountability.

8 — number of countries responsible for 50% of the population growth over the next 30 years (Source)

Connecting the Dots & EIEIO...

Old MacDonald had a farm, EIEIO. New MacDonald has a Startup.... EIEIO: Entrepreneurship, Innovation, Education, Impact and Opportunity. Accordingly, we focus on these key areas of the future.

One of the core goals of GSV is to connect the dots around EIEIO and provide perspective on where things are going and why. If you like this, please forward to your friends. Onward!

Make Your Dash Count!

-MM

Michael Moe is the founder of Global Silicon Valley, as well as the ASU GSV Summit, GSVlabs, the GSV MBA in Entrepreneurship, and numerous other investing, advisory, and media businesses. Author of Finding the Next Starbucks (Penguin Group, 2007), The Global Silicon Valley Handbook (Hachette, 2017), and The Mission Corporation (RETHINK Press, 2021), Michael’s honors include Institutional Investor‘s “All American” research team, The Wall Street Journal‘s “Best on the Street” award, and “one of the best stock pickers in the country” by Business Week. As CEO of GSV, he led pre-IPO investments in Facebook, Twitter, Snap, Dropbox, Chegg, Spotify, and many more.